Digital Banking in Trade Finance: What It Means for Your Business

The way businesses finance international trade has changed fundamentally in the last decade. Where mountains of paperwork, long processing times, and opaque communication once defined cross-border transactions, digital trade finance is replacing those frustrations with speed, transparency, and accessibility. Whether you are an importer looking for payment security or an exporter managing counterparty risk, understanding how technology in trade finance works today can give your business a real competitive edge.

According to recent market research, the global digital trade finance market generated approximately USD 101 billion in 2024 and is forecast to grow to around USD 180 billion by 2034. That growth does not happen in a vacuum; it reflects genuine shifts in how businesses, banks, and regulators are approaching cross-border commerce.

What Is Digital Trade Finance?

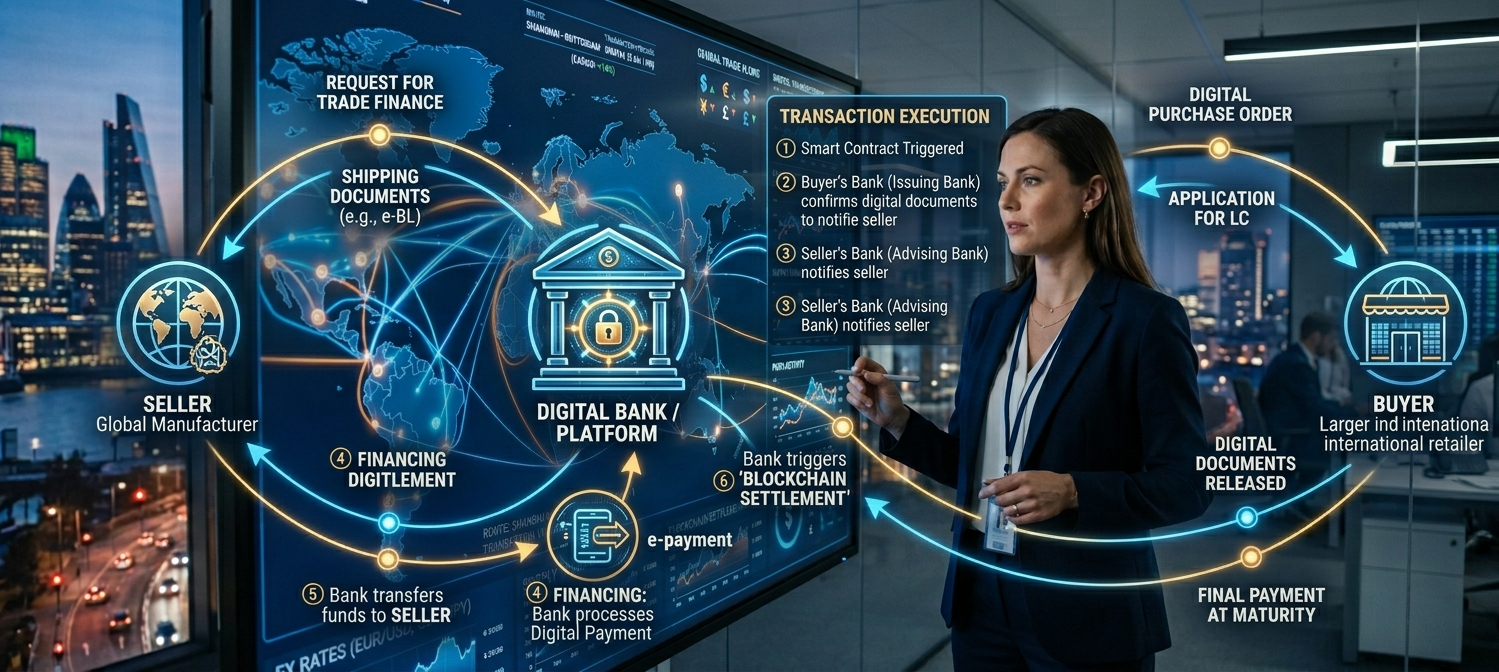

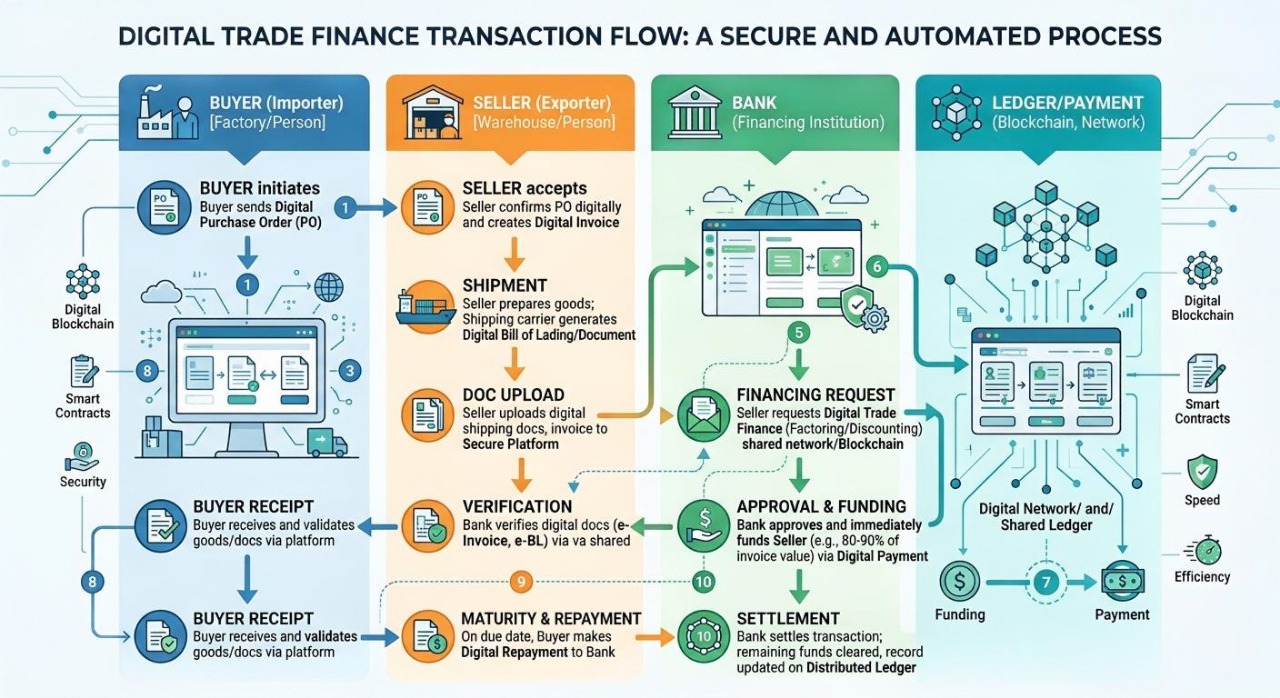

Trade finance has always been about managing risk and providing the liquidity that allows buyers and sellers in different countries to trust each other enough to do business. Traditionally, this relied on physical documents, in-person verification, and lengthy correspondent banking chains.

Digital trade finance applies technology to each of these steps. Electronic documents replace paper. Automated verification replaces manual checks. Cloud-based platforms connect all parties, from importers and exporters to banks and logistics providers, in real time. The result is a faster, lower-cost, and more transparent process that works better for businesses of any size.

Key Technologies Driving Change

Several technologies are at the centre of this transformation and are worth understanding, even at a high level.

Artificial Intelligence and Automation

AI adoption in live trade finance transactions rose from 32% to 45% between 2024 and 2025. This is being used to speed up document verification, assess credit risk in real time, and detect fraud with an accuracy improvement of around 28% compared to older methods. Decision times in trade finance have dropped by up to 35% thanks to AI-powered monitoring systems.

Blockchain

Blockchain technology can cut transaction times by nearly 50% in many trade finance use cases. It creates a shared, tamper-proof record of every step in a transaction, which reduces disputes and builds trust between parties that may have never worked together before. Bank deployment of blockchain in trade finance increased by 22% in 2025, signalling a meaningful shift from pilot programmes to live operations.

Cloud Platforms

Cloud-based trade platforms allow businesses to initiate, track, and manage trade finance instruments from anywhere. Cloud-based platforms supporting digital trade reporting have seen a 35% surge in usage since 2023, reflecting genuine demand from companies operating across multiple jurisdictions.

How Fintech Trade Finance Is Closing the Gap

One of the most pressing problems in global trade is the financing gap. Businesses, especially small and medium-sized enterprises, have historically struggled to access the trade finance instruments they need. Fintech trade finance companies and forward-thinking banks are working to close this gap by making onboarding faster and credit decisions more data-driven. Digital onboarding can reduce SME approval times by up to 40% compared to traditional processes.

This matters enormously for businesses operating in emerging markets or trading across multiple currencies and regulatory environments. Technology in trade finance is making it practical for businesses to access instruments like letters of credit and bank guarantees without the same barriers that existed a decade ago.

Trade Finance Instruments in a Digital World

The core instruments of trade finance have not disappeared with digitalisation; they have simply become easier to access and manage. Here is how the most widely used instruments work in a digital context.

Documentary Letter of Credit

A Documentary Letter of Credit remains one of the most trusted instruments for importers and exporters. It guarantees that payment will be made once the seller presents the required shipping and compliance documents. In a digital environment, the submission and verification of those documents can happen electronically, reducing processing time significantly. Explore our Trade Finance page for more details on how these instruments are structured.

Bank Guarantee

A Bank Guarantee provides assurance to the beneficiary that the bank will cover a loss if a contractual obligation is not met. For contractors, importers, and exporters entering new markets, this is an essential risk mitigation tool. Issued via SWIFT MT760, it carries the full weight of a trusted banking institution behind every transaction.

Standby Letter of Credit

A Standby Letter of Credit (SBLC) functions as a safety net. It is only drawn upon if the applicant fails to meet their obligations, making it a popular tool for long-term business relationships where confidence needs to be established upfront.

Proof of Funds

For high-value transactions, a Proof of Funds document demonstrates to investors or counterparties that the necessary capital is available. In digital trade finance, this can be provided efficiently through verified bank documentation without the delays associated with physical letters.

You can review our full list of applicable Trade Finance Fees and the Jurisdictions & Industries we serve to understand how our digital trade finance capabilities map to your specific business context.

Managing Payments Alongside Trade Finance

A complete digital trade finance solution should also cover how payments are made and received across borders. Our All-In-One Wallet supports transactions in 30+ currencies across 170+ countries, with same-day SWIFT, SEPA, and UK Faster Payments available. For businesses looking to streamline both their trade finance instruments and their day-to-day international payments, this kind of integrated solution removes friction at every stage of the transaction cycle. You can view the All-In-One Wallet Fees and the setup process to get started.

What to Look for in a Digital Trade Finance Provider

Not all digital trade finance platforms are equal. When evaluating a provider, businesses should consider a few core factors.

First, look at the reach and currency coverage. A provider that operates in a limited number of jurisdictions will create bottlenecks as your business grows. Second, consider instrument availability. You want a partner who can issue letters of credit, bank guarantees, and standby LCs through a reputable banking network using SWIFT standards. Third, check transparency on fees. Hidden costs in trade finance can erode the economics of a deal quickly. Finally, assess compliance capabilities. Strong KYC and AML processes protect both your business and your counterparties.

For further reading on how the trade finance landscape is evolving, the International Chamber of Commerce publishes annual global trade finance surveys that provide authoritative insight into market trends and regulatory developments.

Ready to Simplify Your Trade Finance?

Whether you need a Documentary Letter of Credit to secure your next import deal, a Bank Guarantee to support a major contract, or an integrated payment wallet to manage your cross-border transactions, Suisse Bank has the tools and the reach to support your business.

Our digital trade finance solutions are advised globally via SWIFT MT760/MT710, covering 170+ countries and 30+ currencies. Getting started is straightforward: Become a Client today and discover how modern trade finance can work for you.

Frequently Asked Questions

Is digital trade finance safe?

Yes. Digital trade finance platforms use bank-grade encryption, multi-factor authentication, and compliance protocols including KYC and AML screening. In fact, AI-powered fraud detection has improved accuracy by around 28% compared to traditional manual checks, making digital platforms in many respects more secure than paper-based systems.

Can small businesses access digital trade finance instruments?

Absolutely. One of the most significant benefits of fintech trade finance innovation is that it has expanded access for smaller businesses. Digital onboarding and automated credit assessment have reduced approval times by up to 40% for SMEs, making instruments like letters of credit and bank guarantees far more accessible than they were through traditional banking channels.

How long does it take to issue a bank guarantee digitally?

Timelines vary depending on the complexity of the transaction and the documentation required. However, digital processes significantly reduce the time needed compared to traditional paper-based issuance. Blockchain and automated document verification can compress what once took weeks into days in many standard cases.

What is the difference between a Standby Letter of Credit and a Documentary Letter of Credit?

A Documentary Letter of Credit is a primary payment mechanism; the bank pays the seller once compliant documents are presented. A Standby Letter of Credit is a secondary guarantee that is only triggered if the applicant fails to fulfil their contractual obligations. The SBLC functions more like a performance bond, while a Documentary LC is the main settlement tool in a trade transaction.

Do I need a physical office or local residency to access trade finance services?

Not necessarily. Providers like Suisse Bank onboard clients from worldwide jurisdictions without requiring a registered business or residency in any specific country. The digital onboarding process is designed to accommodate businesses and individuals operating across multiple locations