How to Secure Your Cross-Border Digital Transactions

Moving money across borders has never been more common. Businesses trade globally, freelancers get paid from multiple countries, and individuals send funds to family abroad every day. But with that convenience comes a real question: how do you know your money is actually safe when it crosses international lines?

The answer lies in understanding where the risks are and choosing the right payment security solutions from the start.

Why Cross-Border Transactions Carry Unique Risks

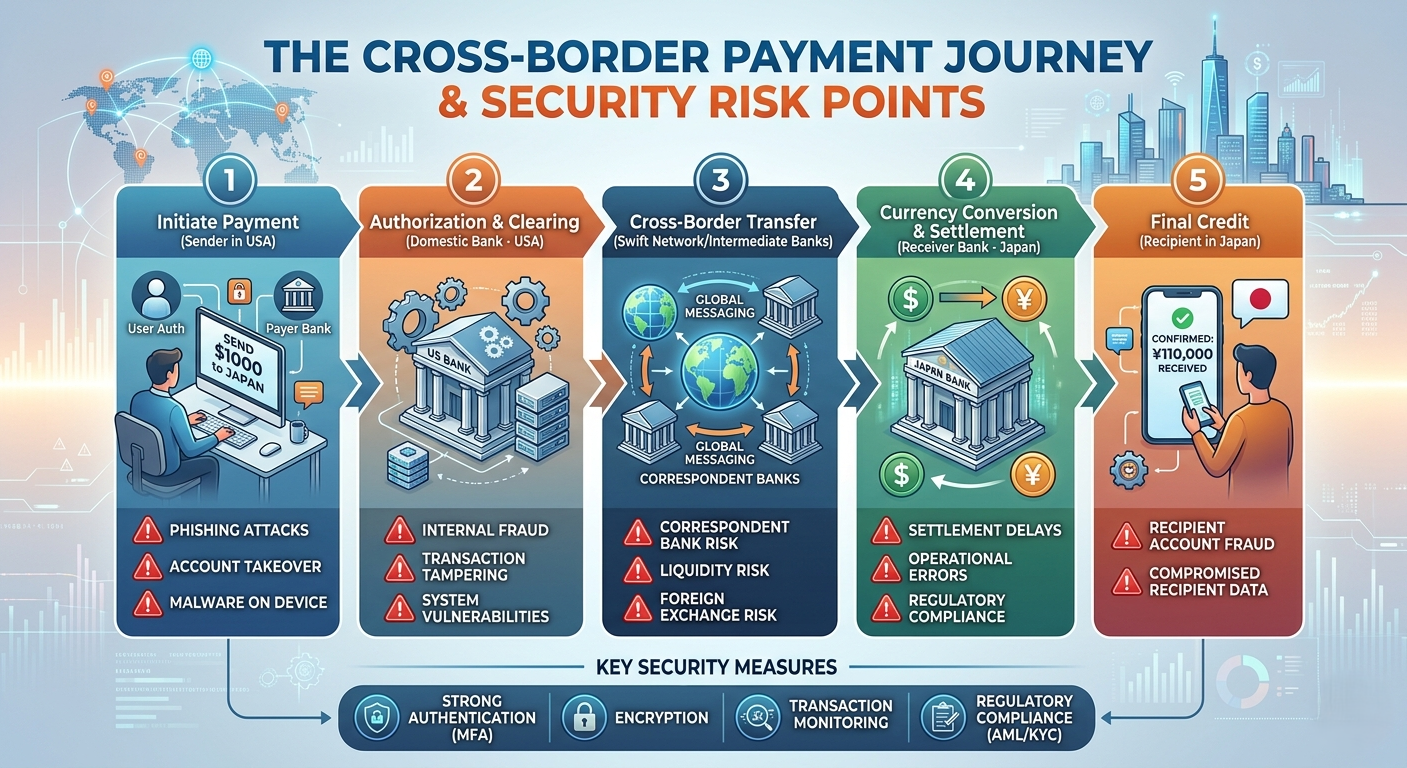

Domestic payments move through familiar, well-regulated systems. International transactions are a different story. They pass through multiple financial networks, often across different legal jurisdictions, different currencies, and varying levels of regulatory oversight.

This creates several vulnerabilities:

Fraudulent interception is more likely when transactions pass through more hands. Currency conversion creates windows for manipulation or errors. Jurisdictional gaps mean that if something goes wrong, recovery can be complicated and slow. Regulatory compliance varies by country, and a transfer that is perfectly legal in one place may trigger scrutiny in another.

These are not hypothetical risks. According to the Financial Action Task Force (FATF), cross-border payment systems are consistently identified as high-risk channels for financial crime, including fraud, money laundering, and sanctions evasion.

That is why the infrastructure behind your payment matters just as much as the payment itself.

The Pillars of Secure Online Transactions

Secure online transactions are not just about having a password. Real security in cross-border payments is built on several layers working together.

Regulatory licensing

Any institution handling your international funds should be properly licensed and regulated. This provides a legal framework for accountability and dispute resolution. Suisse Bank operates within a regulated and compliance-focused framework designed for international financial transactions, you can review it on the License page, which means your funds are handled within a compliant, overseen environment.

Segregated accounts

Your money should be kept separate from operational funds. Suisse Bank's All-In-One Wallet uses segregated accounts, meaning your funds are protected and cannot be mixed with other assets under any circumstances.

Multi-currency infrastructure

Currency conversion is one of the most vulnerable points in cross-border transfers. Having a single, multi-currency account, rather than converting at every step, reduces the number of exchanges and the associated risks. The All-In-One Wallet supports 30+ currencies across 170+ countries in one named account held at a Tier 1 bank in the UK.

Transparent fee structures

Hidden charges are not just a financial issue, they are often a signal of poor transparency, which is a risk factor in itself. Suisse Bank provides full clarity through its All-In-One Wallet Fees page so you always know exactly what you are paying.

Established payment rails

SWIFT, SEPA, SEPA Instant, and UK Faster Payments are the gold standard for international transfers. Using institutions connected to these networks rather than informal or less-regulated channels dramatically improves both security and traceability.

Trade Finance as a Security Mechanism

For businesses involved in international trade, security goes beyond just moving money safely. It means protecting your commercial interests in the transaction itself: ensuring goods are delivered before payment is released, or that contractual obligations are met before funds change hands.

This is where trade finance instruments become genuine payment security solutions.

A Bank Guarantee gives your trading partners confidence that your obligations will be met, reducing the counterparty risk that makes many international deals fall apart before they start.

A Standby Letter of Credit (SBLC) acts as a financial safety net. If one party fails to fulfill its contractual obligations, the SBLC ensures the other party is compensated. It is widely used in international contracts as a form of guaranteed protection.

A Documentary Letter of Credit ties payment to the presentation of specific documents, shipping records, inspection certificates, customs declarations, which means neither buyer nor seller is exposed to risk. Payment only happens when the agreed conditions are verifiably met.

For situations where capital verification is required, such as large investments or real estate transactions in foreign jurisdictions, a Proof of Funds document confirms to all parties that the required capital is available and legitimate.

Suisse Bank issues these instruments globally via SWIFT MT760/MT710 from a trusted institution in the Middle East, giving them the international standing your counterparties expect. You can explore the full range of options on the Trade Finance page, along with detailed Trade Finance Fees.

Compliance and Financial Crime Prevention

Security is not only about technology. It is also about institutional integrity. Suisse Bank maintains a dedicated commitment to Financial Crime prevention, including anti-money laundering (AML) protocols and Know Your Customer (KYC) procedures.

These are not just regulatory boxes to tick. They protect you. When your institution actively screens transactions, verifies counterparties, and monitors for suspicious activity, your money is less likely to get caught up in frozen funds, investigations, or compliance holds that can delay or permanently block access to your own assets.

According to the Basel Institute on Governance, weak AML controls at financial institutions are one of the leading causes of customer fund exposure. Choosing a bank with strong compliance practices is a direct form of financial self-protection.

Ready to Move Money with Confidence?

Cross-border payments carry real risks, but the right infrastructure reduces them significantly. Whether you are an individual managing international finances or a business with active trade relationships, the combination of secure online transactions through a licensed, regulated institution and proper payment security solutions through trade finance instruments is the most reliable path forward.

Suisse Bank offers everything in one place: a multi-currency All-In-One Wallet, complete trade finance instruments, and a compliance framework built for international standards.

Become a Client Today and take control of your international payments with the security they deserve.

Frequently Asked Questions

Q: What is the safest way to send large sums of money internationally?

A: For large international transfers, using bank-grade instruments such as a Standby Letter of Credit or Bank Guarantee offers the highest level of protection because payment is conditional on verified compliance with agreed terms. These instruments are issued through regulated channels like SWIFT and provide legal enforceability across jurisdictions.

Q: How do multi-currency accounts reduce transaction risk?

A: When you hold a single account that natively supports multiple currencies, you avoid repeated conversions between institutions. Each conversion step introduces an exchange rate risk and a potential point of failure. A multi-currency account lets you hold, send, and receive funds in the currency needed without unnecessary intermediary steps.

Q: Does cryptocurrency add security or risk to international payments?

A: Crypto can offer speed and accessibility for certain cross-border payments, but it also adds volatility and regulatory uncertainty depending on the jurisdiction. Using a regulated institution that supports crypto payments and payouts — with proper conversion controls — gives you the flexibility of crypto with the protection of a regulated framework.

Q: What documents are typically needed for a cross-border business transaction?

A: This varies by country and transaction type, but commonly required documents include a commercial invoice, bill of lading or airway bill, certificate of origin, packing list, and in many cases an inspection certificate. Documentary Letters of Credit formalize the use of these documents as payment conditions to protect both parties.

Q: Can I access international banking without being a resident of the UK or having a registered business?

A: Yes. Suisse Bank onboards clients from worldwide jurisdictions regardless of residency or business registration status. You can review which countries and industries are supported on the Jurisdictions and Industries page